In this climate where every other advertisement or banner ad on your Facebook page comes from the financial planning industry, now is a good time to revisit how the traditional financial planning model is irreparably broken.

So many clients of the traditional financial management firms of the world were ecstatic about their investment returns as late as February, but now they are singing the blues — they should be quite disillusioned. It’s not difficult to pick a winner on Wall Street when all of the market is going up up up!

The shortcomings and the fatal flaws of traditional financial planning are now something I hope most people are willing to listen to, consider and ponder. Otherwise so many people who put their entire retirement and hopes for the future will walk through another wall of pain again. Thankfully there is a rise of financial professionals who are coming out and being honest about the fatal flaws of the traditional model of money management. In the list below some hyperbole is used, but be certain that the logic is sound and hits the bullseye 90% of the time.

Let me also say from the outset that my critique is with the financial advisors who are not FIDUCIARIES. They are typically new in the business, not fully licensed, more sales people than advisors. Be careful to not take advice from a salesperson — they have their mind on the sale. I recommend using skilled advisors who are fiduciaries only — this is what you should always demand of any financial planner. This is why it is good to have a team of people – not just one person – on your financial team because they can cross check one another.

I will never give the hand of partnership to the traditional money management industry — instead here is why I suggest you should tell traditional financial advisors to beat it.

THE CLIENT IS NOT FIRST

There is no way to dodge this or sugar coat this. Advisors make their money by selling you what they are told — and only what they are told. Advising a client to purchase something that the advisor can not make a profit from is called “seling away” and is a fireable offense. The reason that the biggest skyscrapers in every city have the names of financial institutions on them is because they have mastered how to market to people their solutions and investments so people think that what they offer is pretty much the only legitimate investments. At every meeting with the traditional advisor, your ability to earn him a commission is one of his highest priorities. For over 100 years this has been their formula of success:

To control as much of your money as possible, to give you back as little as possible, to keep it under their control for as long as possible and to return it to you on their terms and on their time table.

That has been the recipe for success of every bank, investment firm, financial advisor group, insurance company and such and it has worked out well — just look at the skyline of Manhattan or Atlanta. The client is not first — PERIOD

THEY CANNOT OFFER YOU THE BEST SOLUTIONS

They can not offer you the BEST possible solutions. The big traditional firms and the host of other smaller independent brokerages have their hands tied. They have restricted themselves to a very limited number of investment types — typically life insurance, equities (stocks and bonds), and annuities. There is nothing wrong with these tools — in fact, I would argue that no financial tool is in itself bad or harmful; they all have their place and their fit. However when you seek financial guidance you probably want to be shown what is the best fit strategy for your particular situation and retirement hopes.

You will not find this with the traditional advisor. They only have a very limited number of strategies — and those are the ONLY things that they can recommend. For instance, when your situation calls for real estate investing — perhaps owning a rental property for its tax and cash flow benefits — the traditional advisor will not recommend it. In fact, if they did they could be fined and even fired. The term for telling a client to invest their money in an investment that the advisor herself can not sell them — this is called ‘selling away.

Let me put it this way — a vegetarian should never seek dietary advice from a butcher. The butcher will always (and only) recommend meat.

If this is the first time you are hearing this you may think “David, that’s nuts! That can’t be.” I would agree, but it is the case. When a couple or a business owner sits across the table from a traditional advisor, that advisor can ONLY offer them the strategies in his very narrow offerings menu. If you are like me, I would want the advisor to be able to tell me what I need, what is BEST; not simply what he can force into a “best fit” from his bag of investments.

THEY CANNOT OFFER YOU TAX ADVICE

Traditional advisors are not allowed to help you keep your money, that is, from taxes. “We can not give you tax advice,” they say, “because we are not accountants or CPAs.”

(FOR THE RECORD You should always consult a licensed accountant before making any tax decisions.)

So let me get this straight. Most financial experts agree that the biggest expense over your lifetime is taxes (or that it is certainly in the top three).

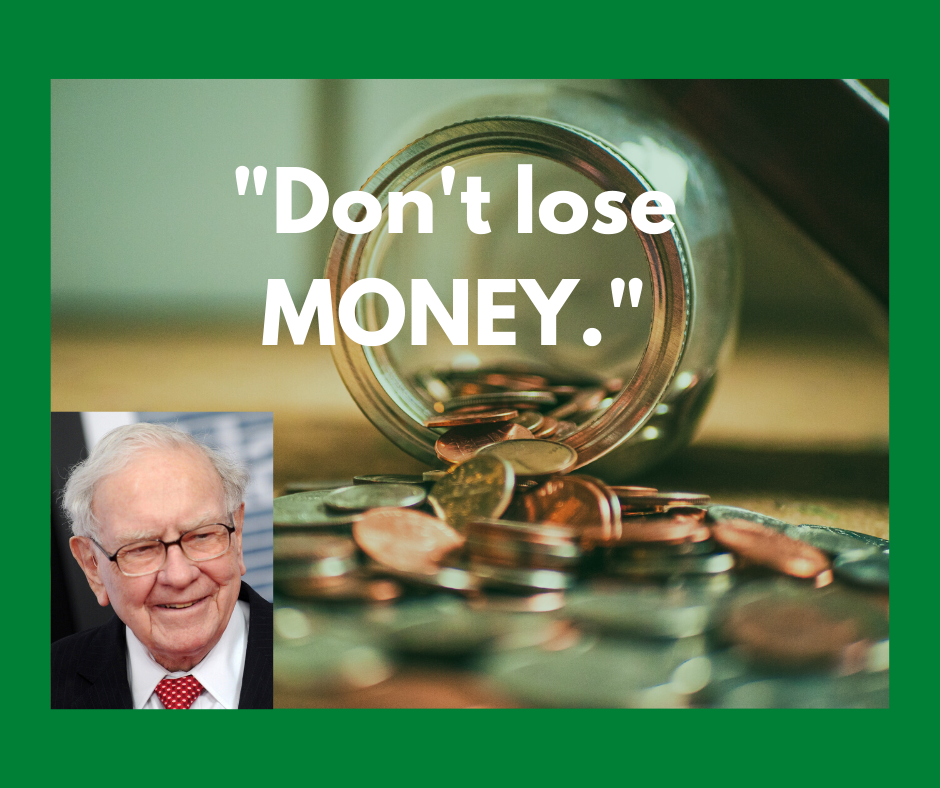

People like Warren Buffet teach that the first rule of wealth building is “don’t lose money.” (By the way, his second rule is “go back to rule #1”).

So the first priority in building wealth can be summed up like this “IT’S NOT HOW MUCH YOU MAKE, IT’S HOW MUCH YOU KEEP.” The traditional advisor then can not help you with this most fundamental aspect of wealth building. They can take your money and invest it for you but they can not tell you how to reduce the very capital gains taxes their investments create.

So that means you are left with going to your accountant, many of whom are not paid to give advice but to file your paperwork. I think this is nuts. This is why it is maddening that so many people mindlessly turn over their money to the traditional financial advisors when in doing so they are losing out on strategies that will help them RETAIN more of their wealth. Tell them to beat it.

They Are Trained To Keep Your Money At All Costs

The traditional financial advisor model is broken. It can not put the client first. It can not offer the best solutions to the client since they are limited to only offer the investments that they have been told to sell. Another reason is that they are trained by their brokers to keep your money under their “management” – by the way, that means control.

Think about it for a moment. If they do not collect a fee for giving you advice how do they make a living? They charge a percentage of the amount of money they ‘control’ or ‘manage.’ So it only makes sense that they are trained to keep you money under their management at all cost (ok, that is a little hyperbole but you get the point).

Do you need to take out some of your funds to buy a rental? You can count on it that your advisor will encourage you to find a different way, maybe question your logic in getting a rental, even offering to “move” some of your money into “something better” like a REIT (real estate investment trust) that he can offer you.

If the market is up and you are making great profits will they advise you to “buy low and sell high”? Will they encourage you to cash in your winnings? Of course not. They are trained to keep you invested — stay in the market. The answer to every question will be some version of “I think you should stay in the market” or “I think you should put more into the market.” This ties into the next reason, which is similar – to a hammer everything looks like a nail.

Despite their best intentions, traditional financial advisors are trained to lead their client back to the same conclusion every time — keep your money with me, keep it in the market, and you are better off not investing outside of what I can offer you. If you win $50,000 in the lottery, and ask them “what should I do with this” they will answer “let me invest it in the market for you.” So what if the market is down? They will reply “well you know the number one rule for investing is to buy low and sell high, so since the market is down let’s buy more stocks while they are on sale!” If the market is on the rise what will they advise? “The market is rising, let’s capture some of those gains.” The answer is always the same – give me more of your extra income to put into the market.

To a hammer everything looks like a nail. Another way of saying this is “if you ask a butcher what is for lunch the answer will always be ‘MEAT.'” (In fact it will be the same answer for breakfast and dinner).

Finally, a personal reason — they don’t like tattoos and social media. Okay, I know that seems a silly. My point is that their model and industry is stuck way back in the twentieth century. They are hammered over and over again by their compliance departments to “beware social media” and they are told that the wrong “post” on Facebook could cost them their job. After a while this shapes a mindset of caution but more importantly of distance from their clients.

Gary Vaynerchuk pointed this out recently to an audience of traditional bankers and advisors — they are guilty of worshipping the past and despising the “new”.

They are trained and hammered to reject anything that smacks of “edgy” or “outside the box” “Tattoos, oh no, that would ruin my relationships, no one would take me seriously as a financial advisor if they knew I had tattoos.” I think this is backward. People want their financial advisors to have a life, to have hobbies, and interests. You want a tattoo to remember your deceased mom then get the tattoo and don’t apologize for it or try to cover it up. It’s what makes you authentic! People want to know who the advisor is when the tie comes off or the heels come off — so they can feel comfortable choosing them to manage their money. Unfortunately, the traditional financial advisor model is trained to avoid creating a “brand” or posting on social media. It’s just business — stuck in the 20th century.

So much of my time is spent helping my clients re-think money to correct some of the wrong ideas they have been told and sold by the traditional financial planning machine. If you would like to know more about how you can grow wealth beyond Wall Street and use strategies and tools that the 1%ers use, reach out to me and let’s have a 12 minute phone call.

*photos by iMattSmart, Alexey Derevtsov